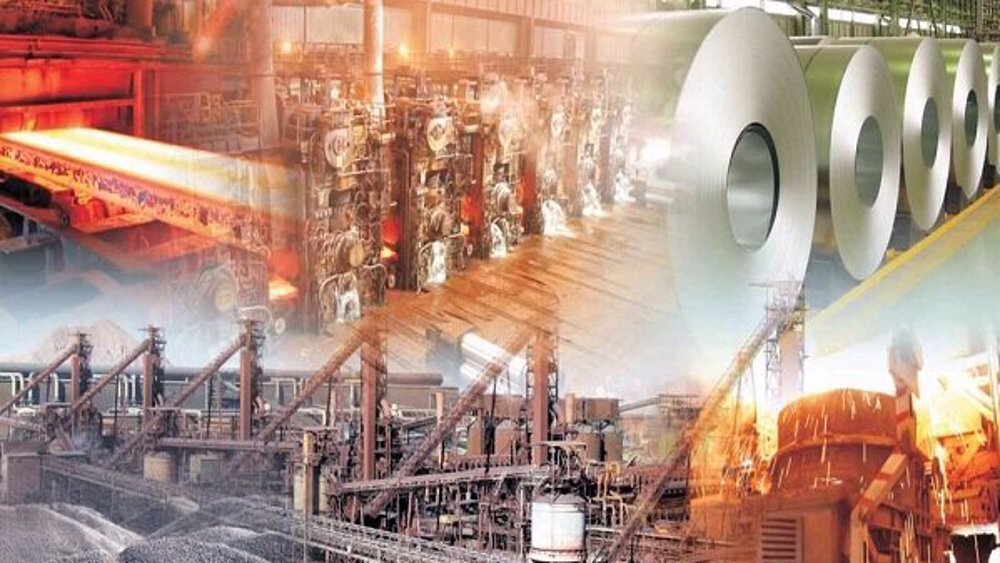

Iran steel holds tenth global ranking despite terrorist US-Israeli attack

In the first quarter of 2026, Iran's steel production reached 7.26 million tonnes, placing it firmly in the tenth position globally.

The World Steel Association, or Worldsteel, released a report claiming that Vietnam, with 6.4 million tonnes produced in the first three months of this calendar year, had snatched Iran’s spot and stood in tenth place.

According to Mehdi Mohammadi, head of the Alloy Steel Producers Association, the Worldsteel report is categorically untrue. Providing further detail, Mohammadi explained that for the period from late December to late March which almost exactly matches the first quarter of 2026, Iran produced 7.26 million tonnes.

Worldsteel simply got it wrong and Iran remains after Brazil with its 8.1 million tonnes, the world’s tenth largest steel producer in the first quarter of 2026.

The achievement underscores not only the sheer scale of Iran's steel industry but also its remarkable ability to withstand and adapt to a critical geopolitical and economic environment.

On April 7, Israel and the United States launched a direct attack on Iran’s steel industry, targeting Mobarakeh Steel and Khuzestan Steel.

The terrorist assault caused considerable disruption, particularly to key facilities like blast furnaces, which led to fears of significant production setbacks.

According to Nader Soleimani, the executive chairman of the Iranian Steel Producers Association, while certain areas have indeed suffered damage, claims of a complete production halt or an inability to meet targets are simply incorrect.

Soleimani insists that relying on domestic capabilities and the successful experience of parts localization, there is confidence that the reconstruction of damaged plants will encounter the fewest possible problems.

Currently, Iran has the capacity to produce about 33 million tonnes of steel. Even so, the capacity utilization rate for Iran’s steelmaking last year was only 63 percent. Steelmakers say if energy restrictions are not imposed on them this year, they will be able to raise their utilization rate and compensate for the loss in the wake of the US-Israeli terrorism.

In other sectors of the steel industry, such as beam and rebar production, plants are operating at full capacity with no serious problems whatsoever.

In areas that have suffered damage, expert estimates indicate that even in the most pessimistic scenario, the reconstruction and return to production will take nine months at most.

Mobarakeh Steel Complex, for example, despite damage in some sections, remains fully active in other areas such as slab production, the raw material for hot-rolled coil, and rolling sections.

The only potential short-term challenge relates to a possible slab shortfall, projected not to exceed 50,000 tonnes per month.

And yet, Mobarakeh’s continued supply on the commodity exchange, including offers of 167,000 to 180,000 tonnes in recent days, suggests relative market stability.

Officials say the only area that might face a shortage is hot-rolled coil production. But the Ministry of Industry, Mine, and Trade has issued import permits to Mobarakeh so that, if needed, this shortage can be compensated.

In recent weeks, certain speculators in the open market, using the pretext of damage to Mobarakeh’s infrastructure in the recent imposed war and creating tensions by alleging steel shortages, have arbitrarily raised prices of related products, including automobiles.

Car prices have seen sharp increases over the past two weeks, with sellers justifying the hikes by claiming a shortage of steel sheets.

On Thursday, Minister of Industry, Mine, and Trade Mohammad Atabak stated at a meeting with automakers, parts manufacturers, and car importers that there is no concern regarding the supply of steel sheets needed for vehicles.

Granted, the shadow of war and sanctions may affect production trends. But technical capabilities and domestic manufacturing provide reassurance.

It is expected that with a reduction in tensions, damaged steelmaking plants, including Mobarakeh, will quickly return to production. Iran has proven this ability before.

In 2018, US President Donald Trump sanctioned Iran’s steel industries, but that became a turning point for localization of industrial parts.

At the time, the steel industry’s dependence on imported parts consumed about $4.5 billion of the country’s foreign currency annually.

With the imposition of sanctions and a ban on parts sales, Iran summoned knowledge−based companies and domestic manufacturers and launched a massive project to localize 26,000 parts needed by the steel industry.

The Ministry of Industry, Mine, and Trade and mines and metal holding company IMIDRO supported this self−sufficiency drive by banning registration of orders for imported localized parts. This measure not only prevented currency outflow but also allowed domestic manufacturers to grow and flourish.

Today, the currency consumption for supplying steel production line parts has dropped from $140–145 to about $45–50. That means fabricated domestic components from furnaces to converters to auxiliary installations are all produced inside the country.

Iran today is not merely a steel producer but also an exporter and has managed to maintain its tenth global ranking. The country is engaged in a war of wills, where the enemy’s strategic mistake in attacking infrastructure cannot break the will of the Iranian nation.

Total steel production before the revolution stood at about one million tonnes per year. After the Islamic Revolution in 1979, despite the imposed war and enormous economic difficulties, the country managed to increase steel production by about 400,000 tonnes to reach 1.2 million tonnes annually.

Subsequently, the first five-year steel development plan was formulated to increase steel production by one million tonnes every year. At the end of the plan, the country’s steel production reached 7.5 million tonnes per year.

That post-revolution war of wills also led to the formulation of development plans, including the 2025 Vision Plan, which set a target of producing more than 55 million tonnes of steel annually.

Having secured a tenth-place global ranking ahead of countries such as France and Italy, Iran has held its position through a proven combination of technical self-reliance and rapid post-attack recovery.

The attack on Mobarakeh and Khuzestan was meant to break that momentum. Instead, it has become yet another chapter in a long record of turning external pressure into industrial strength.

The untold story of hidden war on Iran's dinner table

Iran localizes 2,000 sanctioned petrochemical components to boost domestic production

Iran's homegrown aerospace industry takes wing with Simorgh

US Army depletes long-range missile stockpile in war of aggression against Iran: Report

Iran-Oman Hormuz corridor talks progress despite US obstruction, source tells Press TV

Iraq’s PMU mobilizes massive security force for Arbaeen procession

VIDEO | Anti-Trump protests sparked Flamingo Revolution in Albania

Millions of Iranians mark Arbaeen, call for vengeance for martyred Leader

Israeli settler detained for alleged espionage for Iranian intelligence agencies

South Korean police detain students after protest at US air base

British academic and Press TV co-host David Miller wins landmark appeal in anti-Zionism case